You got a dividend.

Then came the question you didn’t expect: do I pay tax on this?

Unfortunately, it is not a yes or no answer. It depends on which account — TFSA, RRSP, or non-registered — you’re holding the investment in, and whether that dividend came from a Canadian company or a foreign one like the U.S.

We will cover the most common scenarios a Canadian investor is likely to run into. If you’re still figuring out what a dividend actually is, start with What Is a Dividend in Canada?, then come back here.

This article covers how dividends are taxed in Canada. The examples use federal tax rates only. Each province also has its own dividend tax credit on top — the rates will vary depending on where you live.

By Capital Corner Editorial Team | Last updated: June 29, 2026 | 6-minute read

.jpg)

How Do Canadians Earn Dividends?

To earn a dividend, you need to own stock in a company that pays one — or an ETF that holds dividend-paying stocks.

Some companies share a portion of their profits with investors on a regular basis. That payment is called a dividend. Not every company pays one — Shopify and Lululemon, for example, don’t. But many large, well-established Canadian companies do — think banks like TD and RBC, or companies like Enbridge and Canadian National Railway. If you own stock in one of those, or an ETF that holds them, dividends are likely already coming your way.

Eligible vs. Non-Eligible Dividends in Canada — What’s the Difference?

Not all Canadian dividends are taxed the same way. There are two types: eligible and non-eligible.

Eligible dividends come from publicly traded Canadian companies — the kind listed on the stock exchange. The big banks, major energy companies, established telecoms. If you’re buying stocks or ETFs through a brokerage, this is almost certainly what you have.

Non-eligible dividends usually come from private Canadian businesses. If you own part of a small business or private company, this is where you’d see them. Different rules, different situation — and not what most new investors are dealing with.

For the rest of this article, we’re focused on eligible dividends. That’s what most Canadians have in their accounts.

TFSA, RRSP, or Non-Registered — How Each Account Is Taxed on Canadian Dividends

Before we get into how much tax you owe, there’s one question that matters more than anything else: where are you holding your investments?

The answers below apply to Canadian dividends. U.S. dividends play by a different set of rules — we cover those in their own section below.

TFSA — If your dividend-paying stocks or ETFs are inside a TFSA, you owe nothing. The dividend lands in your account tax-free. No T5 slip. No math. Done.

RRSP — Canadian dividends inside an RRSP grow without being taxed while they sit there. You pay tax when you eventually take the money out.

Non-registered account — This is where tax comes into play. If your investments are here, you do owe tax on Canadian dividends.

What Is the Canadian Dividend Tax Credit and How Does It Work?

The dividend tax credit is a break the government gives you on your tax bill when you receive dividends from a Canadian company. It exists because that money was already taxed once before it reached you.

When a Canadian company makes a profit, it pays corporate tax before it pays you your dividend. For eligible dividends, that corporate tax gross rate is 38%.

Say the company earned $1,000 in profit. At 38% corporate tax, they paid $380 in tax. That left $620. Out of that, they paid you a $200 dividend.

When that $200 reaches you, the CRA adds that 38% back before calculating your tax. So your $200 becomes $276.

And yes — it feels strange. You only received $200, so why are you reporting $276?

That’s a fair question.

The gross-up is only half the story. Next comes the dividend tax credit, which helps reduce the tax you owe because the company already paid tax before the money reached you.

Does it completely cancel out the gross-up? No. But it does lower your tax bill.

The important thing to remember is this: the gross-up and the dividend tax credit work together. Looking at one without the other makes the system seem a lot worse than it usually is.

Here’s what that same $200 dividend looks like using a sample tax rate of 26%:

At first glance it looks like the system is working against you. But once the dividend tax credit kicks in, you’re actually keeping more than you would on the same amount of employment income — $169.70 versus $148.00. Dividends are still worth it.

One more thing worth knowing: your province also has its own dividend tax credit on top of the federal one. Every province is different, which is why your final tax bill depends on where you live. Your T5 slip and your tax software handle both credits automatically when you file.

How Are U.S. Dividends Taxed in Canada?

If you own U.S. stocks or ETFs, here’s something that catches a lot of people off guard. When a U.S. company pays you a dividend, the U.S. government takes 15% before the money ever reaches you. So on a $100 dividend, you receive $85. That 15% is called withholding tax.

Then at Canadian tax time, you report the full $100 as income and pay tax at your regular rate.

Canada has a separate credit for this type of situation. It’s called the foreign tax credit. Unlike the Canadian dividend tax credit, it’s not a percentage calculation. It’s a direct offset — if you paid $15 to the U.S., you can usually claim the whole $15 against what you owe the CRA. No gross-up. Just a dollar-for-dollar reduction.

One more thing worth knowing: U.S. dividends must be reported in Canadian dollars. Your brokerage converts this for you — but the number on your tax slip may look different from what landed in your account. A $100 U.S. dividend at a 1.35 exchange rate shows up as $135 Canadian on your slip. That’s the number you report as income.

Quick recap: Canadian dividends get the dividend tax credit. U.S. dividends get the foreign tax credit. Different stocks, different rules, different credits.

Best Account for Dividend Stocks in Canada — TFSA, RRSP, or Non-Registered?

TFSA — Canadian dividends are completely tax-free. No tax, no reporting, no T5 slip.

U.S. dividends are a different story. The 15% withholding tax still applies, and you cannot get it back. That $15 is gone every time.

RRSP — Canadian dividends grow inside the RRSP without being taxed while they sit there. Just keep in mind that when you eventually take the money out, it comes out as regular income. At that point, the dividend tax credit doesn’t apply.

U.S. dividends are the opposite story — the RRSP is actually the best place for them. Under the Canada-U.S. tax treaty, the U.S.

recognizes the RRSP as a retirement account, so the 15% withholding is waived. Your full $100 arrives.

Non-registered account — Canadian dividends are taxed, but at a lower rate thanks to the dividend tax credit we covered above.

U.S. dividends have the 15% withheld up front, but you can claim the foreign tax credit when you file to get most of it back.

This is also the only account that generates a T5 slip. If all your investments are inside a TFSA or RRSP, you won’t receive one.

Dividend Reinvestment Plan (DRIP) Tax Rules in Canada

A DRIP — Dividend Reinvestment Plan — automatically takes your dividend and uses it to buy more stock instead of paying you cash. If you’re not familiar with how a DRIP works, we cover it in What Is a Dividend in Canada?

In a TFSA or RRSP, this isn’t an issue. DRIP away.

But there’s a catch if you’re running a DRIP in a non-registered account. In the CRA’s eyes, whether you received your dividend as cash or as more stock, they treat it the same. You still owe tax on it.

Your T5 slip will show it.

What If Your ETF Pays Dividends?

A lot of Canadians start investing with ETFs rather than individual stocks — and ETFs can pay dividends too. The same rules apply. The account you hold your ETF in determines what you owe.

Also realize that just because you bought a Canadian EFT, doesn’t mean all the stocks inside it are Canadian.

If you own an ETF that holds a mix of Canadian and U.S. stocks, don’t worry about sorting it all out yourself. The ETF does that for you. You’ll receive one tax slip — usually called a T3 — and it will show everything broken down: your Canadian dividends, your U.S. or other foreign dividends, and any withholding tax that was applied.

How to Report Dividend Income in Canada — T5 and T3 Slips

If you earn dividends in a non-registered account, your bank or broker sends you a T5 slip by the end of February or a T3 by the end of March. A copy goes to the CRA automatically.

The slip shows everything you need — your actual dividend amount, the grossed-up amount, whether it was Canadian or U.S., and any tax credits that apply. Enter the box numbers into your tax software. It does the rest.

If all your investments are inside a TFSA or RRSP, you won’t receive a slip at all.

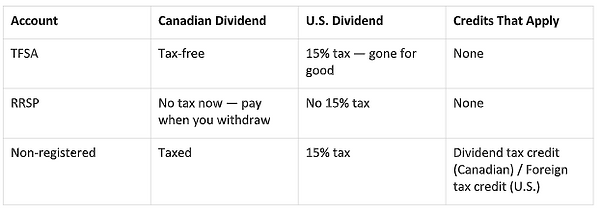

Quick Reference — Canadian vs. U.S. Dividends by Account

Here’s a quick cheat sheet to keep it all straight.

Bottom Line

Whether you owe tax on a dividend comes down to two things: where it came from and where you’re holding it.

Canadian dividends in a TFSA are tax-free. Everything else involves some tax — but credits exist to make sure you’re not paying more than your share.

When tax season arrives, your T5 or T3 slip has everything you need. Enter the numbers into your tax software and it handles the rest.

Get Started Today

☐ Check where your dividend-paying investments are held — TFSA, RRSP, or non-registered account

☐ If you own U.S. stocks or ETFs, check which account they’re in — this affects whether the 15% tax applies

☐ If you have a non-registered account, watch for your T5 or T3 slip by the end of February or March

☐ Enter your slip numbers into your tax software — it handles the math from there

Frequently Asked Questions

Q: Do I have to report dividends if I didn’t get a T5 slip?

Yes. If you earned dividends in a non-registered account, you are required to report them even if you didn’t receive a slip. This can happen if you earned less than $50 in dividends, from the company or brokerage paying you. Check your brokerage account or log into CRA My Account — both will show what you were paid during the year.

Q: Can I earn Canadian dividends tax-free in a non-registered account?

Sometimes, yes. It depends on your income level. The lower your income, the more likely the dividend tax credit wipes out what you owe completely. Your tax software calculates this automatically when you file.

Q: How much of a U.S. dividend do I actually keep in a non-registered account?

Here’s how it plays out on a $100 U.S. dividend.

The U.S. withholds 15% before the money reaches you, so you receive $85. At Canadian tax time, at a mid-range tax rate of around 26%, you would owe another $11 to the CRA.

Total tax paid: $26. You keep: $74.

But that’s before your provincial tax applies.

This is your worst case scenario for U.S. dividends — a non-registered account with no tax planning. But there are better options, like holding U.S. dividend stocks in an RRSP. Not sure what an RRSP is? See What Is an RRSP in Canada?

Disclaimer

The information on Capital Corner is for educational purposes only and does not constitute financial, tax, investment, or legal advice. Always consult a qualified professional before making financial decisions.

Affiliate Disclosure

Capital Corner may earn a commission from links on this page, at no extra cost to you. We only recommend products and services we believe are genuinely useful to our readers.